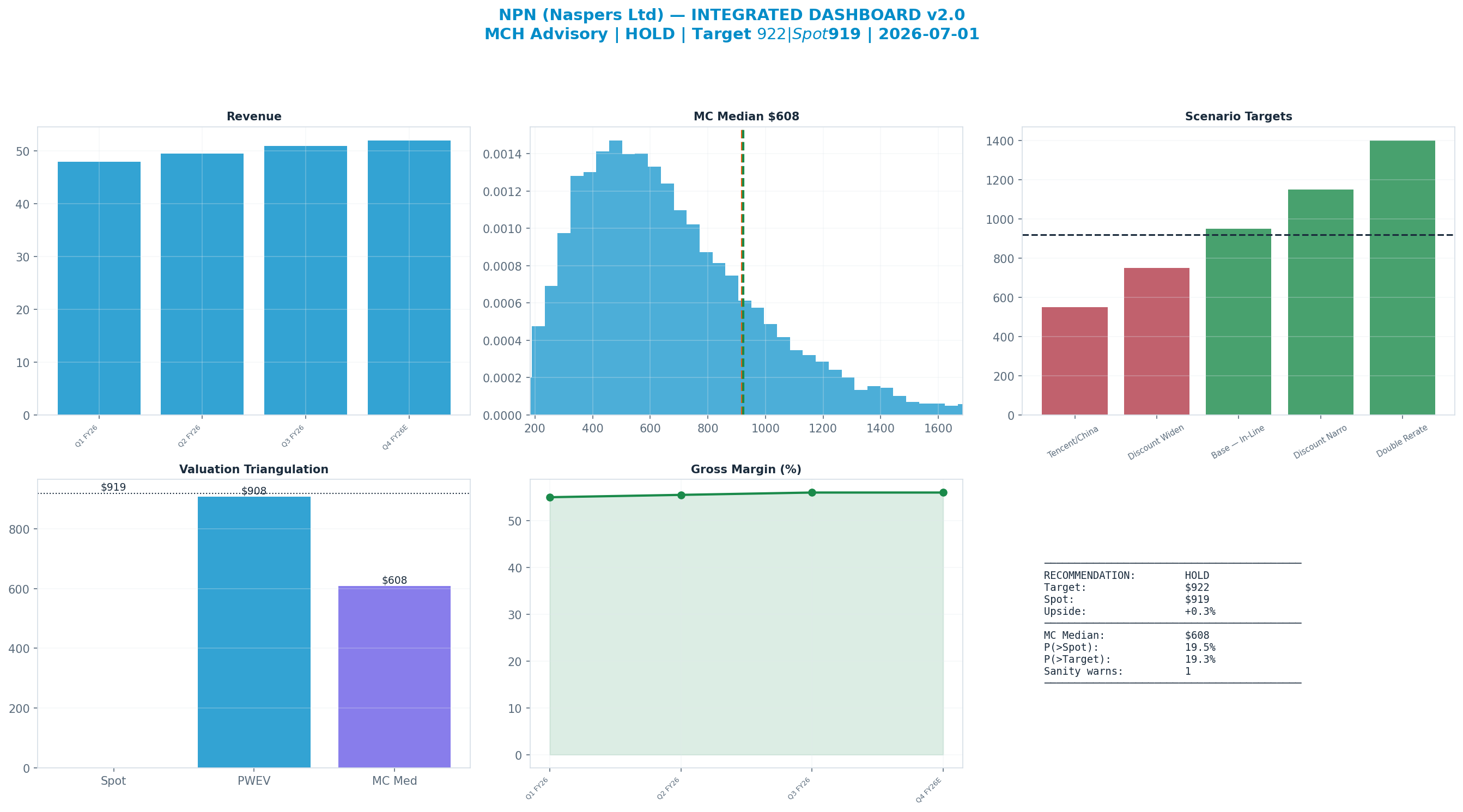

Rating: HOLD

| Metric | Value |

|---|---|

| Current Price | $919 |

| Triangulated Fair Value | $795 |

| 12-mo Scenario PWEV | $908 |

| Implied Return | -14% |

| Market Cap | $698B |

| 52-Week Range | $838 – $1,311 |

Methodology: Valuation triangulated across five independent anchors — Monte Carlo (Student-t + regime switching), an independent DCF, peer re-rating, a sum-of-parts, and a scenario-weighted PWEV. Figures reconciled to JSE 2026-04-15 (ZAc). Each chart below sits with the part of the thesis it evidences.

Investment Thesis

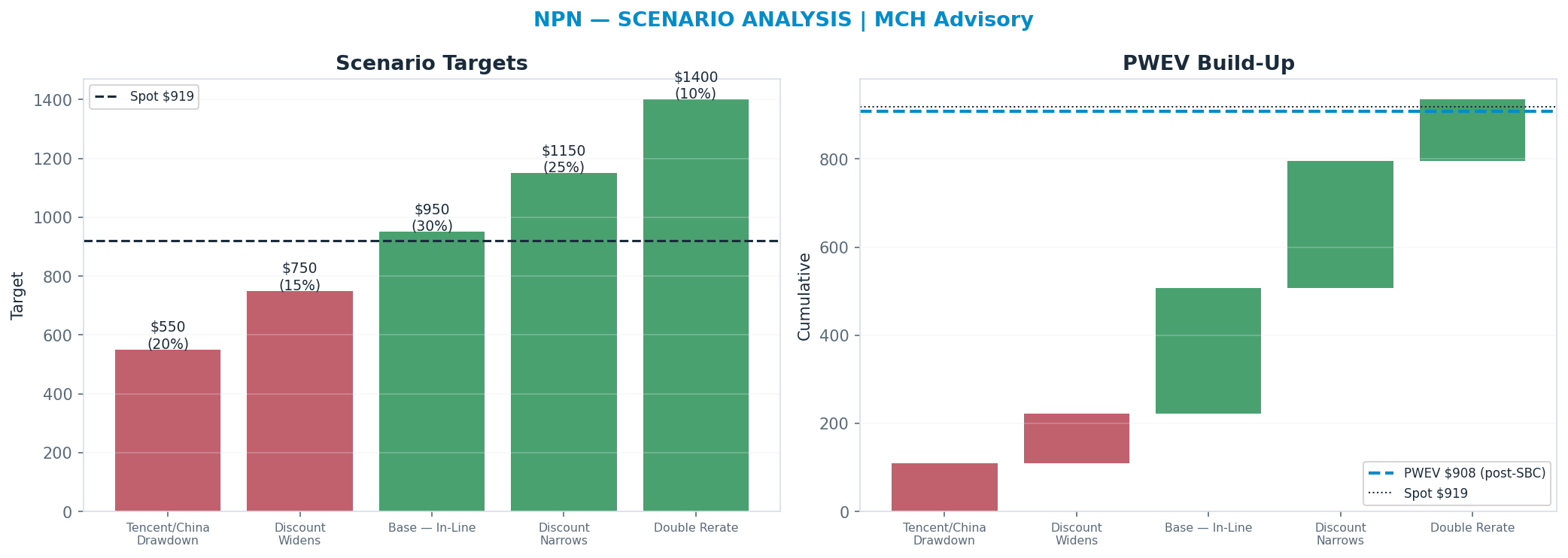

The bull case — 'Double Rerate' (10% weight) — targets $1,400, +52% vs spot. It needs the multiple to hold or expand.

The dashboard below is the whole argument on one page: spot ($919) against each valuation anchor, the scenario tree, technicals and the options-implied move.

Anti-Thesis (The Real Bear Case)

The structural case — 'Tencent/China Drawdown' (20%) — targets $550, -40% vs spot. This sits below the 52-week low — a genuine structural impairment, not a mild pullback.

Key Debate

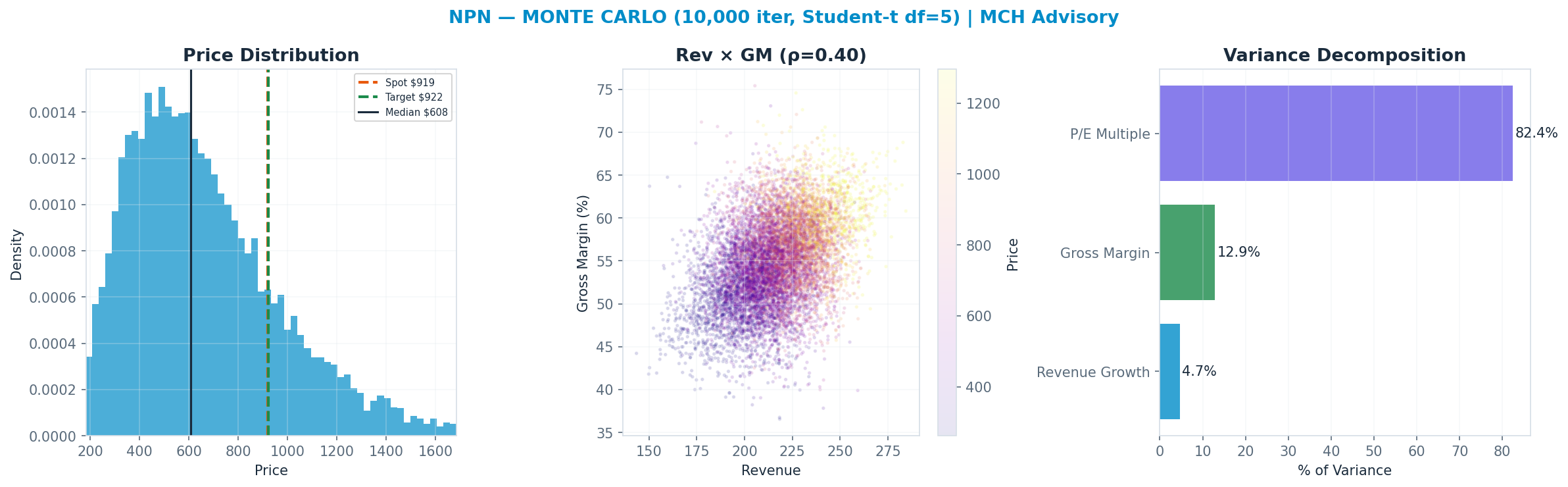

P/E Multiple explains 82% of Monte Carlo outcome variance — i.e. value is set by the multiple the market will pay, a rate/sentiment regime bet as much as an earnings bet.

Scenario Analysis

The tree runs from a structural 'Tencent/China Drawdown' downside ($550) to a 'Double Rerate' bull case ($1,400); the probability-weighted blend (PWEV $908) is -1% versus spot.

| Scenario | Probability | Target | Return |

|---|---|---|---|

| Tencent/China Drawdown | 20% | $550 | -40% |

| Discount Widens | 15% | $750 | -18% |

| Base — In-Line | 30% | $950 | +3% |

| Discount Narrows | 25% | $1,150 | +25% |

| Double Rerate | 10% | $1,400 | +52% |

| Probability-Weighted (PWEV, after SBC dilution) | — | $908 | -1% |

SBC charge: scenario targets are gross per-share prices; the PWEV is reduced by one year of stock-based-compensation dilution (3.0% of shares), trimming the gross PWEV of $935 to $908 (-2.9%). SBC is charged once, as dilution — never also deducted from FCF.

Valuation Triangulation

Five anchors — but read them with their basis in mind. The Monte Carlo, the DCF terminal, and the peer re-rate all key off a market multiple, so they are not fully independent; only the discounted cash flows themselves are genuinely multiple-free. The discipline is to read the spread and weight the cash-based view, not to treat five numbers as five independent votes.

| Method | Basis | Fair Value | vs Spot |

|---|---|---|---|

| Monte Carlo median (Student-t + regime) | multiple | $608 | -34% |

| Scenario PWEV | multiple | $908 | -1% |

| Triangulated (weighted) | — | $795 | -14% |

Monte Carlo — the distribution, not a point

10,000 paths, Student-t shocks (fat tails) with a regime-switching overlay. The median lands at $608 and 19% of paths finish above spot. The variance decomposition shows the p/e multiple is the dominant swing factor (82% of variance). Value is a multiple bet: fundamentals move the answer far less than the rating does.

Across all anchors the spread is tight (the methods corroborate one another).

Load-Bearing Assumptions

No DCF anchor is meaningful for this asset; the blend leans 62% on probability-weighted scenarios and 37% on the Monte Carlo median — the scenario probabilities are the load-bearing inputs.

Reasons the Thesis Could Fail (Falsifiable)

P(>current)=19.5% below 30% band — bear weighting or opex may be too severe; verify. The valuation is multiple-dependent (82% of variance); a de-rating toward the Monte-Carlo anchor ($608) implies -34%.

Fact / Inference / Speculation

- FACT: Spot $919; 52-week range $838–$1,311; engine rating HOLD; base-case target $922 (+0%).

- INFERENCE: Triangulated FV $795 (-14%). P/E Multiple explains 82% of Monte Carlo outcome variance — i.e. value is set by the multiple the market will pay, a rate/sentiment regime bet as much as an earnings bet.

- SPECULATION: At current prices the embedded bet is that the multiple holds or expands — P/E Multiple carries 82% of outcome variance.

Recommendation: HOLD

Balanced: triangulated fair value $795 (-14% vs spot); the outcome hinges on P/E Multiple. The debate is P/E Multiple (82% of variance) — fundamentally a multiple/regime call. SBC runs —M TTM (disclosed in the appendix).