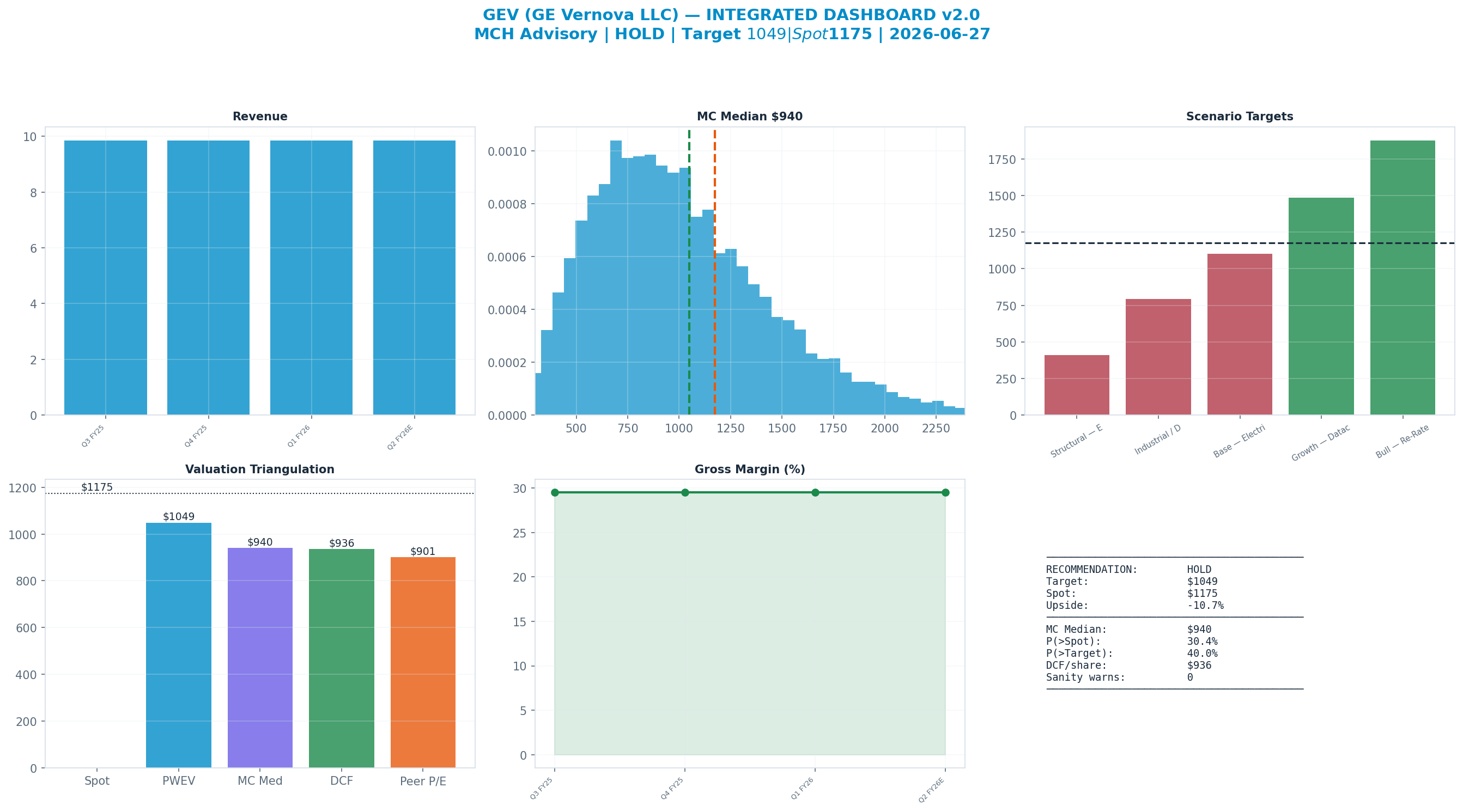

Rating: HOLD

| Metric | Value |

|---|---|

| Current Price | $1,175 |

| Triangulated Fair Value | $966 |

| 12-mo Scenario PWEV | $1,049 |

| Implied Return | -18% |

| Forward P/E | 43.7x |

| Market Cap | $329B |

| 52-Week Range | $481 – $1,181 |

Methodology: Valuation triangulated across five independent anchors — Monte Carlo (Student-t + regime switching), an independent DCF, peer re-rating, a sum-of-parts, and a scenario-weighted PWEV. Figures reconciled to Alpha Vantage 2026-06-27. Each chart below sits with the part of the thesis it evidences.

Investment Thesis

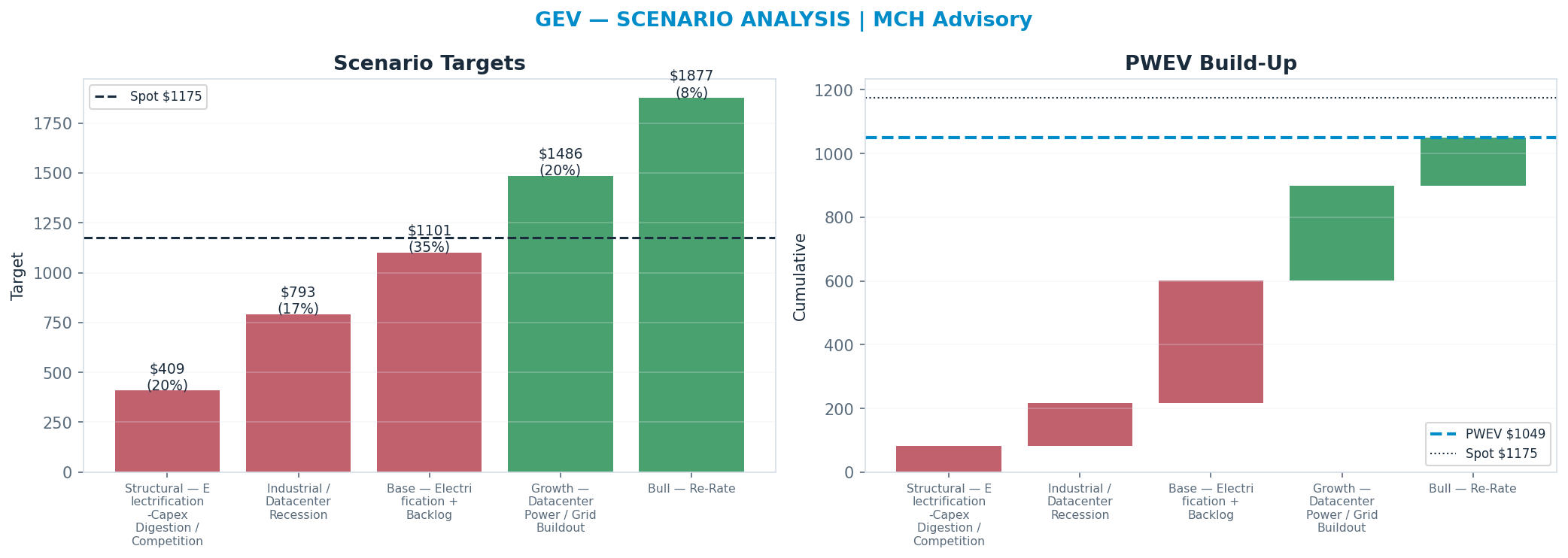

The bull case — 'Bull — Re-Rate' (8% weight) — targets $1,877, +60% vs spot. It needs the multiple to hold or expand.

The dashboard below is the whole argument on one page: spot ($1,175) against each valuation anchor, the scenario tree, technicals and the options-implied move.

Anti-Thesis (The Real Bear Case)

The structural case — 'Structural — Electrification-Capex Digestion / Competition' (20%) — targets $409, -65% vs spot. This sits below the 52-week low — a genuine structural impairment, not a mild pullback.

Key Debate

P/E Multiple explains 66% of Monte Carlo outcome variance — i.e. value is set by the multiple the market will pay, a rate/sentiment regime bet as much as an earnings bet.

Earnings-Call Disconfirmation & Sentiment

Derived signals from the MCH market-data store (Alpha Vantage transcripts + news). Quantitative tone only — a disconfirmation flag, not a substitute for reading the call.

Management vs analyst tone (2026Q1): management +0.49 vs analyst floor +0.26 → delta +0.24 (n=18 mgmt / 7 Q&A; 19th pctile across the S&P book, z -0.9).

Flag: TYPICAL — management-vs-analyst tone within the normal cross-sectional range.

| Quarter | Mgmt | Analyst | Delta |

|---|---|---|---|

| 2026Q1 | +0.49 | +0.26 | +0.24 |

| 2025Q4 | +0.46 | +0.24 | +0.22 |

| 2025Q3 | +0.66 | +0.19 | +0.47 |

| 2025Q2 | +0.39 | +0.23 | +0.16 |

News (last 365d, 1000 articles): avg ticker sentiment +0.28 (bullish 30% / bearish 1%)

Scenario Analysis

The tree runs from a structural 'Structural — Electrification-Capex Digestion / Competition' downside ($409) to a 'Bull — Re-Rate' bull case ($1,877); the probability-weighted blend (PWEV $1,049) is -11% versus spot.

| Scenario | Probability | Target | Return |

|---|---|---|---|

| Structural — Electrification-Capex Digestion / Competition | 20% | $409 | -65% |

| Industrial / Datacenter Recession | 17% | $793 | -33% |

| Base — Electrification + Backlog | 35% | $1,101 | -6% |

| Growth — Datacenter Power / Grid Buildout | 20% | $1,486 | +26% |

| Bull — Re-Rate | 8% | $1,877 | +60% |

| Probability-Weighted (PWEV) | — | $1,049 | -11% |

Scenario rationale — what each probability buys (the driver path behind every target):

- Structural — Electrification-Capex Digestion / Competition (20%, $409). Structural impairment — electrification-capex digestion / competition: earnings AND the multiple compress together. Target sits below the 52-week low by construction. Drivers — implied_target: 408.76; probability: 0.2.

- Industrial / Datacenter Recession (17%, $793). Cyclical downturn — electrification + datacenter power + grid/utility capex + industrial automation weakens for 1–2 years before normalising. Drivers — implied_target: 792.55; probability: 0.17.

- Base — Electrification + Backlog (35%, $1,101). Mid-cycle — normalised electrification + datacenter power + grid/utility capex + industrial automation; disciplined capital allocation; steady returns. Drivers — implied_target: 1100.76; probability: 0.35.

- Growth — Datacenter Power / Grid Buildout (20%, $1,486). Upside — datacenter power + grid buildout lifts earnings above mid-cycle; the multiple expands modestly. Drivers — implied_target: 1486.02; probability: 0.2.

- Bull — Re-Rate (8%, $1,877). Upside tail — sustained tight conditions or a structural re-rate on datacenter power + grid buildout. Drivers — implied_target: 1876.79; probability: 0.08.

Valuation Triangulation

Five anchors — but read them with their basis in mind. The Monte Carlo, the DCF terminal, and the peer re-rate all key off a market multiple, so they are not fully independent; only the discounted cash flows themselves are genuinely multiple-free. The discipline is to read the spread and weight the cash-based view, not to treat five numbers as five independent votes.

| Method | Basis | Fair Value | vs Spot |

|---|---|---|---|

| Monte Carlo median (Student-t + regime) | multiple | $940 | -20% |

| Peer P/E re-rate | multiple | $901 | -23% |

| Peer EV/Revenue re-rate | multiple | $823 | -30% |

| Scenario PWEV | multiple | $1,049 | -11% |

| DCF (5-year + terminal) | cash flow + terminal × | $936 | -20% |

| Triangulated (weighted) | — | $966 | -18% |

Rating vs blend — the key debate. The rating tracks the multiple-discipline fair value (Monte Carlo $940 + scenario PWEV $1,049, ≈ spot); the weighted blend $966 (-18%) sits below it because the cash-flow DCF ($936) is materially more conservative than the market multiple. Whether the current multiple is justified is the central question for this name — and the principal downside risk to the rating.

Monte Carlo — the distribution, not a point

10,000 paths, Student-t shocks (fat tails) with a regime-switching overlay. The median lands at $940 and 30% of paths finish above spot. The variance decomposition shows the p/e multiple is the dominant swing factor (66% of variance). Value is a multiple bet: fundamentals move the answer far less than the rating does.

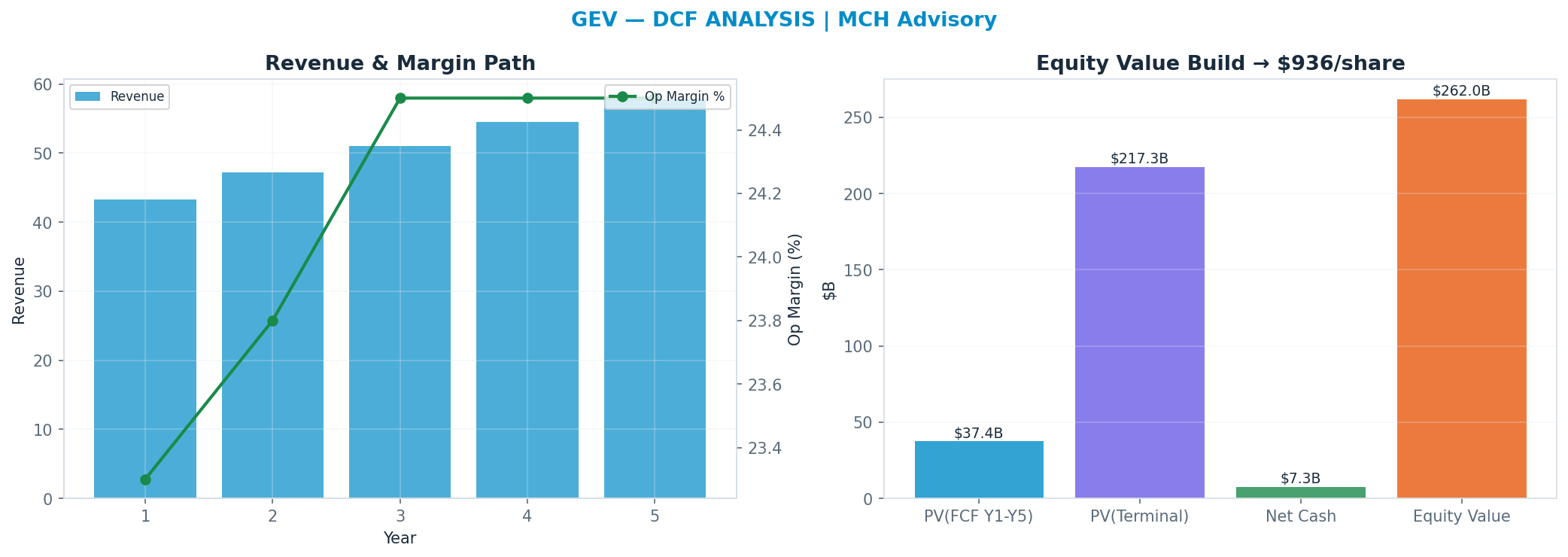

DCF — the cash-flow anchor

Independent of the market multiple: a 5-year path, WACC 9.0%, 30x terminal FCF multiple → $936. This anchor is deliberately the heaviest (41%): it is the valuation least hostage to the current multiple regime.

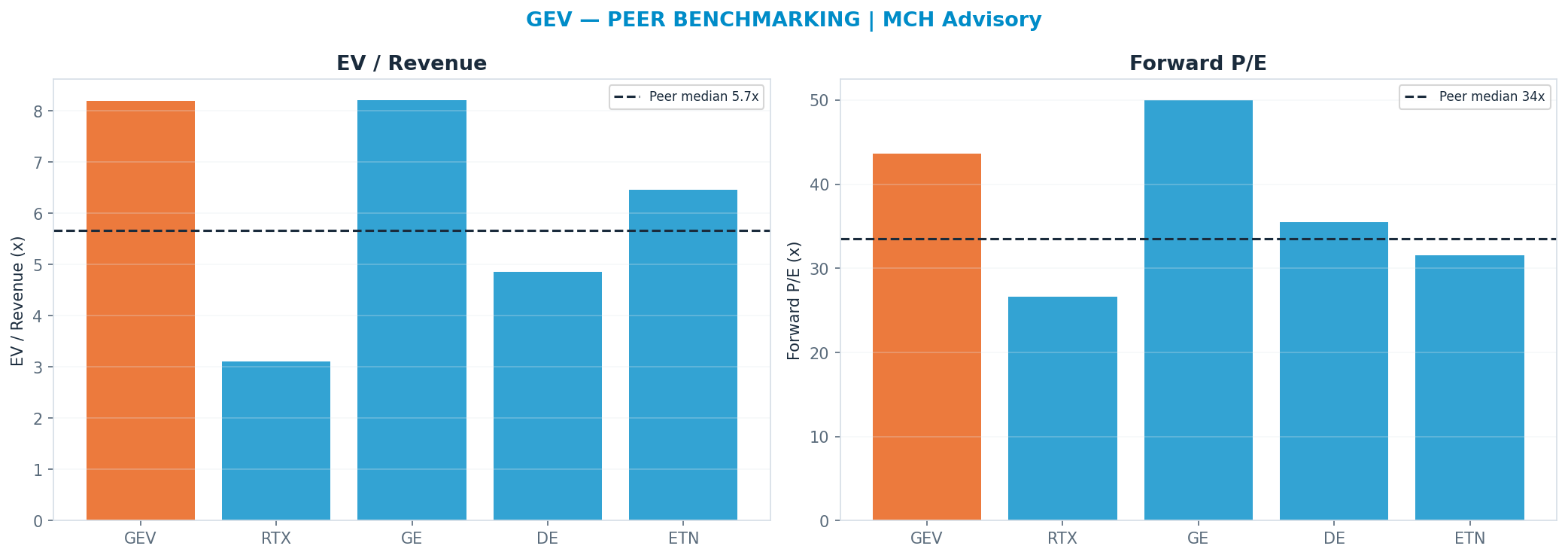

Peer benchmarking — relative value

Against the peer cohort, re-rating to the peer-median forward multiple (P/E 33.505x) implies $901. A premium is only justified by superior growth/margins; otherwise it is multiple risk. Weighted just 12% so the market's mood does not drive the fair value.

Across all anchors the spread is tight (the methods corroborate one another).

Revenue-Segment Breakdown

The company-specific drivers behind the valuation — each segment carries its own growth, margin, multiple and capex intensity. (Tags: FACT reported · ESTIMATE from disclosures · INFERENCE judgment.)

| Segment | Revenue | Mix | Growth | Op margin | Multiple | Capex % | Tag |

|---|---|---|---|---|---|---|---|

| Electrical Equipment & Power | $39.4B | 100% | 10% | 22% | 39x | 4% | ESTIMATE |

Named Exposures

Demand & pricing cycle (FACT/ESTIMATE)

| Dimension | Assessment |

|---|---|

| driver | electrification + datacenter power + grid/utility capex + industrial automation |

| net_debt_or_cash_b | 7.32 |

Capital intensity & shareholder returns (ESTIMATE)

| Dimension | Assessment |

|---|---|

| capex_pct_revenue | 0.04 |

| div_yield | 0.0014 |

Structural risk vs optionality (INFERENCE)

| Dimension | Assessment |

|---|---|

| downside | electrification-capex digestion / competition |

| upside | datacenter power + grid buildout |

Industry Context — Ind Electrical

This name sits in the Ind Electrical as a electrical_equipment. electrification + datacenter power + grid/utility capex + industrial automation Its scenarios are not guessed in isolation — they inherit a single, shared view of the cluster's driver cycle, so the names that depend on the same event are mutually consistent.

Value chain: GEV (electrical_equipment) · ETN (electrical_equipment) · VRT (electrical_equipment) · EMR (electrical_equipment) · AME (electrical_equipment) · ROK (electrical_equipment) · GNRC (electrical_equipment)

| Shared state | Capex path | House view | This name implies |

|---|---|---|---|

| Electrification-Capex Digestion / Recession | 37% | 37% | |

| Mid-Cycle — Electrification + Backlog | 35% | 35% | |

| Upside — Datacenter Power / Grid Buildout | 28% | 28% |

On the cluster's key downside — Electrification-Capex Digestion / Recession () — this name implies 37% vs the cluster house view of 37% (in line with the house). The cluster's full cross-stock reconciliation governs that the names which ride the same capex cycle assign it comparable odds.

Structure: Shared State — The ind_electrical cycle is the shared macro driver. Driver — electrification + datacenter power + grid/utility capex + automation Dispersion — Members differ by cyclicality (quality compounders vs deep cyclicals).

Model Appendix

DCF — line items

| Year | Revenue | Op income | − Capex | + D&A | FCF | PV(FCF) |

|---|---|---|---|---|---|---|

| FY+1 | $43B | $10B | $2B | $2B | $8B | $8B |

| FY+2 | $47B | $11B | $2B | $2B | $9B | $8B |

| FY+3 | $51B | $12B | $2B | $2B | $10B | $8B |

| FY+4 | $55B | $13B | $2B | $2B | $11B | $7B |

| FY+5 | $58B | $14B | $2B | $2B | $11B | $7B |

| Terminal | — | — | — | — | $11B × 30x | $217B |

FCF is bridged: NOPAT + D&A − Capex − ΔNWC (capex intensity 4% of revenue, weighted from the segments) — not a single conversion fudge.

WACC 9.0% · Σ PV(FCF) $37B + PV(terminal) $217B = EV $255B; + net cash → equity $262B ÷ diluted shares 0.28B = $936/share (exit-multiple terminal).

- Gordon (perpetuity-growth) terminal at 2.5% → $568/share — a genuinely non-multiple, cash-based cross-check; the exit-multiple and Gordon values bracket the terminal-value risk.

- Incremental ROIC on the forecast capex ≈ 33% vs WACC 9% → above WACC — the build is value-creative.

Peer set

| Peer | EV/Rev | Fwd P/E | Growth | Op margin |

|---|---|---|---|---|

| RTX | 3.113x | 26.6x | 7% | 13% |

| GE | 8.21x | 50.0x | 7% | 20% |

| DE | 4.86x | 35.46x | 3% | 18% |

| ETN | 6.46x | 31.55x | 10% | 16% |

| Median | 5.66x | 33.505x | — | — |

Peer-median fwd P/E → $901; EV/Rev → $823.

Weighted fair-value math

| Anchor | Value | Weight | Contribution |

|---|---|---|---|

| DCF | $936 | 41% | $385 |

| Scenario PWEV | $1,049 | 29% | $309 |

| Monte Carlo median | $940 | 18% | $166 |

| Peer P/E | $901 | 12% | $106 |

| Triangulated | — | 100% | $966 |

Sensitivity

DCF/share — WACC × terminal multiple

| WACC \ Term× | 21.0x | 25.5x | 30.0x | 34.5x | 39.0x |

|---|---|---|---|---|---|

| 7% | $763 | $891 | $1,019 | $1,147 | $1,274 |

| 8% | $732 | $854 | $976 | $1,098 | $1,220 |

| 9% | $703 | $819 | $936 | $1,052 | $1,169 |

| 10% | $675 | $786 | $898 | $1,009 | $1,120 |

| 11% | $649 | $755 | $861 | $968 | $1,074 |

DCF/share — revenue CAGR Δ × op-margin Δ

| CAGRΔ \ MgnΔ | -3.0pp | -1.5pp | +0.0pp | +1.5pp | +3.0pp |

|---|---|---|---|---|---|

| -3.0pp | $731 | $781 | $832 | $882 | $932 |

| -1.5pp | $775 | $829 | $882 | $936 | $990 |

| +0.0pp | $821 | $878 | $936 | $993 | $1,051 |

| +1.5pp | $870 | $931 | $992 | $1,053 | $1,115 |

| +3.0pp | $921 | $986 | $1,051 | $1,117 | $1,182 |

Tornado — DCF/share swing by driver (widest first)

| Driver | Low | High | Swing |

|---|---|---|---|

| Terminal × ±15% | $819 | $1,052 | $233 |

| Op margin ±3pp | $821 | $1,051 | $230 |

| Revenue CAGR ±3pp | $832 | $1,051 | $219 |

| WACC ±1pp | $898 | $976 | $79 |

| FCF conversion ±10% | $936 | $936 | $0 |

Company lever — SoP/share vs Electrical Equipment & Power multiple (AI re-rating) (base 39x)

| Multiple | 27.3x | 33.1x | 39.0x | 44.8x | 50.7x |

|---|---|---|---|---|---|

| SoP/share | $3,868 | $4,684 | $5,514 | $6,330 | $7,160 |

Load-Bearing Assumptions

DCF: WACC 9%, terminal multiple 30×, FY+5 revenue $58B. Triangulation leans 41% on DCF, 29% on PWEV.

Reasons the Thesis Could Fail (Falsifiable)

The valuation is multiple-dependent (66% of variance); a de-rating toward the DCF anchor ($936) implies -20%.

Fact / Inference / Speculation

- FACT: Spot $1,175; 52-week range $481–$1,181; engine rating HOLD; base-case target $1,049 (-11%).

- INFERENCE: Triangulated FV $966 (-18%). P/E Multiple explains 66% of Monte Carlo outcome variance — i.e. value is set by the multiple the market will pay, a rate/sentiment regime bet as much as an earnings bet.

- SPECULATION: At current prices the embedded bet is that the multiple holds or expands — P/E Multiple carries 66% of outcome variance.

Recommendation: HOLD

Balanced: triangulated fair value $966 (-18% vs spot); the outcome hinges on P/E Multiple. The debate is P/E Multiple (66% of variance) — fundamentally a multiple/regime call. SBC runs —M TTM (disclosed in the appendix).